Importers must purchase a number of emissions certificates (CBAM certificates) that corresponds to the emissions of the CBAM goods they import. The number of certificates to be purchased is based on the embedded emissions of imported CBAM goods, with one CBAM certificate corresponding to one tonne of emissions. This section describes the various factors that are taken into account when calculating the number of certificates.

The starting point for calculating the number of CBAM certificates is information obtained from the manufacturer about the emissions generated in the manufacture of the goods. Alternatively, you can use the default value, published by the Commission, to represent the emissions of the goods in question.

One CBAM certificate corresponds to one tonne of CO2e (tCO2e). However, when calculating the number of certificates, certain deductions are made from the emissions due to adjustments. In other words, the calculation takes into account

- the adjustment due to the emissions allowances allocated free of charge in the EU Emissions Trading System (EU ETS)

- the carbon price, if any, paid in a non-EU country.

The number of certificates to be purchased is not adjusted as regards the electricity imported.

Free allocation under the EU ETS will be phased out

Some of the emissions allowances under the EU ETS have been allocated free of charge to emission-intensive sectors to prevent carbon leakage. The free allocation of EU ETS allowances will be phased out over the period 2026–2034 and replaced by the Carbon Border Adjustment Mechanism (CBAM). The costs of purchasing the CBAM certificates will gradually rise as the free allowances are phased out.

The number of EU ETS allowances allocated free of charge is calculated at installation level using EU ETS benchmarks, whereas the corresponding free allocation adjustment under the CBAM is applied at goods level. Therefore, the CBAM benchmarks used when calculating the adjustment are defined according to commodity code.

If actual emissions data have been used in the annual declaration, the free allocation adjustment must reflect the actual manufacturing process and composition of the goods. If default values have been used in declaring the emissions, the adjustment must likewise be based on the default CBAM benchmark values for free allocation.

When default values are used in the annual declaration, the origin of the input materials (precursors) and the composition of the goods are taken into account when selecting the CBAM benchmark. If actual values are used, the actual production routes at the installation are taken into account.

If you’re using default emission values in the annual declaration, the CBAM benchmark is also selected based on default values. The benchmark value is selected from the values provided in point 5.3 of the Annex to the implementing regulation on the calculation of the number of CBAM certificates while considering the default production route of the goods. The Annex contains separate CBAM benchmark values depending on whether actual emissions data or default values are used in the annual declaration. The country-specific default production route has been defined in the annexes to Regulation (EU) 2025/2621 on default values.

The CBAM benchmark values are based on the ETS benchmark values to be used over the period 2026–2030 to ensure uniform treatment of imports. The CBAM benchmark values published by the Commission reflect, as far as possible, the ETS benchmark values for the period 2026–2030. These CBAM benchmark values will be reviewed as soon as the new ETS benchmark values are published. The final CBAM benchmark values will become applicable on 1 January 2027.

How the free allocation adjustment affects the calculation of CBAM certificates

The free allocation adjustment affecting the calculation of the number of CBAM certificates involves taking into account the quantity of imported goods, the CBAM factor and the CBAM benchmark. The calculation is also affected by the cross-sectoral correction factor for the total amount of EU ETS allowances allocated free of charge. The free allocation adjustment is calculated as specified in point 2 of the Annex to Implementing Regulation (EU) 2025/2620 regarding the calculation of the number of CBAM certificates.

The free allocation adjustment reduces the number of CBAM-certificates that are needed. The reducing effect is calculated using three different factors:

- CBAM benchmark

- CBAM factor

- cross-sectoral correction factor.

The CBAM benchmark reflects the average emissions of the ten most emission‑efficient installations in the EU. CBAM benchmarks are defined by commodity code, and they take into account the production route and material composition of the goods. The CBAM benchmarks are published in point 5.3 of the Annex to the Implementing Regulation on the calculation of the number of CBAM certificates. They take into account the default production route for the production of the goods concerned. Separate benchmarks have been defined for actual emissions data and for default values.

The CBAM factor is the percentage for the gradual phase‑out of free allocation of EU ETS allowances, and it is determined according to the year of import. The CBAM factor will gradually decrease over the years 2026–2034. The CBAM factors have been published in article 10a(1a) of Directive 2003/87/EC on emission allowance trading within the Union. You can also find a table listing the CBAM factors in this guidance under “Example of how the number of certificates is calculated using default values”.

The cross-sectoral correction factor is also linked to the free allocation of EU ETS allowances. Each year, it adjusts the quantity of allowances for each allocation period. At the moment, the cross-sectoral correction factor is set as 1, that is, 100%. We will inform our customers if the factor changes.

How the carbon price affects the calculation of CBAM certificates

The carbon price only can be deducted in the calculation of CBAM certificates if it has actually been paid in a non-EU country.

If default values have been used, the deduction of the carbon price can only be requested based on the annual default carbon prices. The Commission will set the available default carbon prices, and they will be published in the CBAM Registry in 2027.

Include the precursors in the calculation for complex goods

When using actual emissions data for complex goods, the calculation of the number of CBAM certificates must also take into consideration the free allocation adjustment for each relevant input material (precursor). Complex goods are goods produced using other CBAM goods. Default values specific for the country and production route can be used in the calculation for the embedded emissions of one or more precursors.

Example of how the number of certificates is calculated using default values

The embedded emissions are declared using either actual emissions data or default values. For iron, steel, aluminium, hydrogen and electricity, only direct emissions are declared. In the cement and fertiliser sectors, both direct and indirect emissions are declared.

When using default values for the emissions, you must take into account the country of origin and production route of the goods.

- On its CBAM website, the Commission has published the default values and benchmarks for the definitive period in Excel format under “Default values and benchmarks for the definitive period”.

Example: You have declared 900 tonnes of aluminium bars for release for free circulation. The bars originate in Indonesia and belong to commodity code 7604 29 10. To calculate the number of CBAM certificates needed, you must find out the default emissions value for the commodity code, the CBAM benchmark value, the cross-sectoral correction factor and the default carbon price.

First, let us find out the default emissions value. Open the Implementing Regulation (EU) 2025/2621 on default values, where you can find a table in Annex I containing country-specific default values by CN code.

The table shows the default value for direct emissions first, then the default value for indirect missions and, in the last columns, the total default value of these emissions, for which an annual mark-up has been defined. The marked-up default values are used in the annual declaration. That is, in 2026, the default value for aluminium bars is 2.266 tCO2e/t. The default value for 2027, in turn, is 2.472 tCO2e/t.

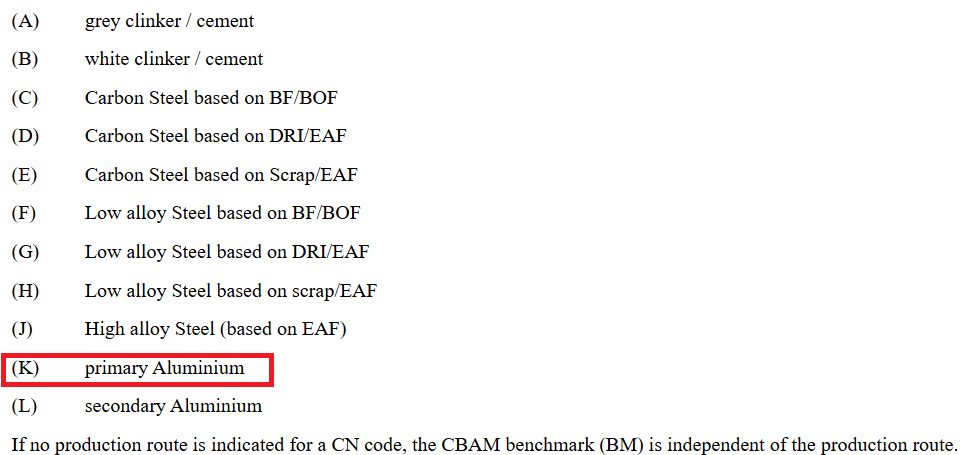

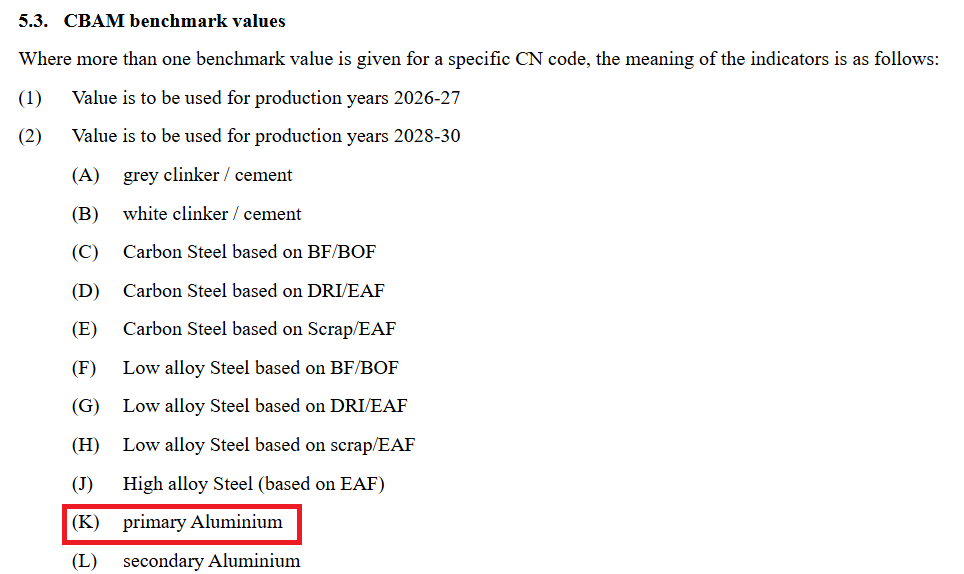

The production route determining the CBAM benchmark is primary aluminium (K), which is shown in the last column of the table.

The letters identifying the different production routes can be found at the beginning of Annex I.

If you do not know the country of origin of the goods or if the default values for the country of dispatch do not contain the commodity code, you should use the default values under “Other countries and territories” in Annex I.

Next, we must find out the CBAM benchmark value. Open the Implementing Regulation (EU) 2025/2620 on calculating the number of CBAM certificates. There are descriptions at the beginning of point 5.3 of the Annex that decide the choice of benchmark when more than one benchmark value is given for a specific CN code. The choice of benchmark value may be influenced by the year of production (1–2) and production route (A–L).

Column A of the table shows the values for the actual emissions data and column B shows the default values.

You have imported aluminium bars belonging to CN code 7604 29 10 from Indonesia. The production route is primary aluminium (K). The aluminium bars were manufactured in 2026. Default values are used in the annual declaration, so the benchmark value is selected from column B. As regards aluminium bars, the benchmark value in column B has not been provided for a specific production year. Therefore, the benchmark value in this case is 1.485 (K, or primary aluminium). The benchmark value is chosen based on the production route defined for the CN code in the default value table.

When the benchmark value has been found, you still need to find out the CBAM factor for the year of import for the calculation. The CBAM factors have been published in article 10a(1a) of Directive 2003/87/EC on emission allowance trading within the Union. You can find the factors in the following table:

| 2026 | 97,5 % |

| 2027 | 95,0 % |

| 2028 | 90, 0 % |

| 2029 | 77,5 % |

| 2030 | 51,5 % |

| 2031 | 39,0 % |

| 2032 | 26,5 % |

| 2033 | 14,0 % |

| 2034 | 0,0 % |

The aluminium bars were manufactured in the year 2026 and released for free circulation in the EU territory the same year, so the CBAM factor for that year is 97.5%.

The last factor needed for calculating the number of certificates is the cross-sectoral correction factor, which is 1 (= 100%) in 2026. In other words, the correction factor does not affect the calculation for the year 2026, so it does not need to be included in this example.

In the example case, a carbon price has been paid for the emissions in Indonesia in 2026. As we are using the default emission values, we must also use the default value for the carbon price. Let us imagine that the default carbon price published by the Commission for Indonesia is 20 €/tCO2e in this example.

We use €85 as the price of a CBAM certificate in this example.

We have now established the values needed for calculating the number of CBAM certificates required for the goods (commodity code 7604 29 10, country of origin Indonesia, and mass 900 tonnes):

- specific embedded emissions based on default values, 2.266 tCO2e/t

- CBAM benchmark value for the production route in accordance with the default value, 1.485 tCO2e/t

- CBAM factor, 97.5%

- carbon price paid in the country of origin according to the default price, 20 €/tCO2e

- price of a CBAM certificate, €85.

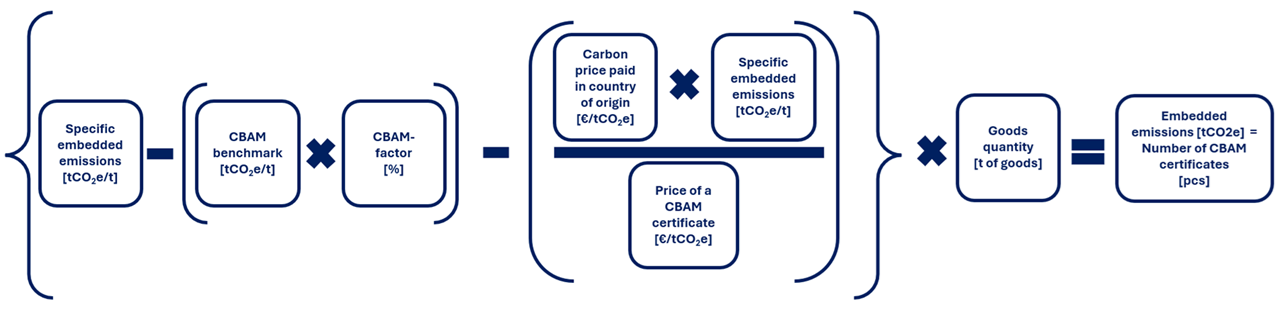

Firstly, we calculate the deduction due to the free allocation adjustment by multiplying the CBAM benchmark value (1.485) with the CBAM factor (0.975). The product of the multiplication is 1.448 tCO2e/t.

After this, we calculate the deduction due to the carbon price paid. The carbon price paid in the country of origin (€20) is multiplied with the embedded emissions (2.266). The product of this multiplication is 45.32, which is divided by the price of a CBAM certificate (€85). The resulting figure is 0.533 tCO2e/t.

Next, we subtract these deductions from the embedded emissions (2.266 – 1.448 – 0.533), and as a result, we arrive at the adjusted emission value 0.285 tCO2e/t.

Finally, this adjusted emission value is multiplied with the mass of the goods in tonnes (0.285 x 900), and we arrive at the result 256.5. That is, the number of CBAM certificates to be purchased is 257. As the price of a CBAM certificate in this example is €85, the CBAM cost for the import amounts to a total of 257 x €85 = €21 845.

Adjustment for precursors when using actual emissions data

When using actual emissions data for complex goods in the annual declaration, the calculation of the number of CBAM certificates must, beside the adjustment for the finished CBAM goods, also take into consideration the free allocation adjustment for each relevant precursor material. Complex goods are goods produced using other CBAM goods.

In practice, the free allocation adjustment is calculated for each precursor by multiplying the CBAM benchmark with the CBAM factor.

The adjustment for the precursors is apportioned to the specific mass consumption of the precursor, that is, to how big a mass of the precursor has been spent in proportion to the mass of the goods made in the next step of the manufacturing process.

Example: 100 tonnes of goods is manufactured. During the production, 80 tonnes of a precursor has been consumed. The specific mass consumption is calculated by dividing the quantity of precursor consumed (80 tonnes) with the quantity of goods produced (100 tonnes). The resulting ratio is 0.80 (80%). The free allocation adjustment for this precursor is multiplied by this ratio.

If the installation produces complex goods using precursors of a certain type that originate from several different installations, a weighted average is used when calculating the free allocation adjustment for these precursors. The weighted average gives the figures included in the calculation a different weight when calculating the average.

Example: The installation uses a precursor from two other installations that belongs to the same commodity code. The final goods are manufactured so that 30% of the precursor used comes from the first installation and 70% from the second installation. Based on this, the free allocation adjustment for the precursor belonging to the commodity code should be made up of a 30% adjustment calculated using the benchmark for the production route of the first installation and a 70% adjustment calculated using the benchmark for the production route of the second installation.