Goods traffic between Åland and mainland Finland

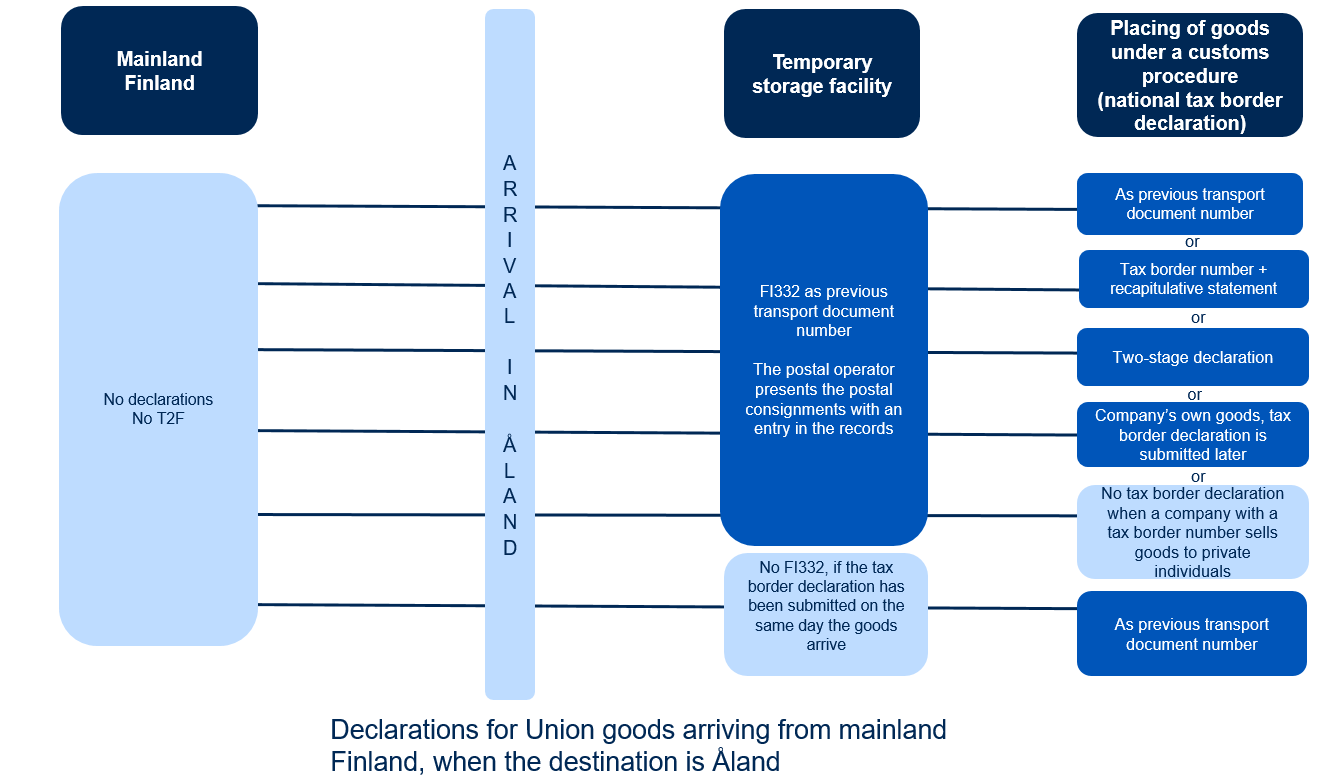

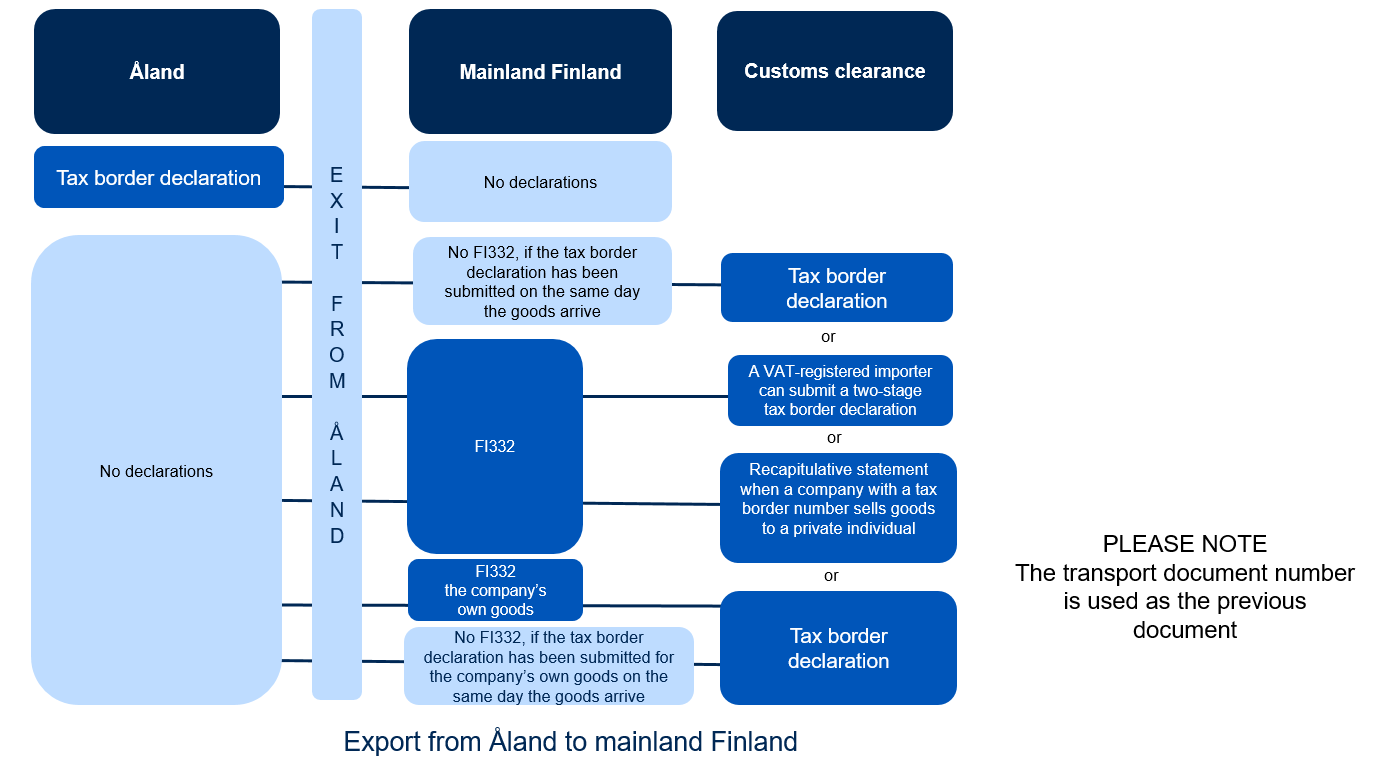

All goods transported from Åland to mainland Finland or from mainland Finland to Åland must be presented to Customs, and a national tax border declaration (customs declaration) must be submitted for them.

Presentation notification

- The person importing the goods across the tax border must present the arriving goods to Customs using a presentation notification, or, alternatively, using the customs declaration, in which case a separate presentation notification is not required.

- You can use a representative to submit the presentation notification.

Read more about the presentation notification

National tax border declaration (customs declaration)

The importer must submit a customs declaration for goods transported across the tax border between Åland and mainland Finland.

A company registered for VAT can submit the declaration in two stages or in one stage.

The importing company is responsible for submitting the declaration even if they use a representative to submit it.

Read more about the tax border declaration

Recapitulative statement for tax border customers (customs declaration)

- VAT-registered companies that sell goods to private individuals or to organisations or companies not registered for VAT can apply for status as tax border customers.

- Tax border customers submit the import declaration as a recapitulative statement on behalf of the private individual.

- The tax border customer acts as the exporter and is responsible for submitting the declarations.

Read more about applying for tax border customer status and the recapitulative statement